Happy May!

So many good things are happening right now. First, it’s spring, and the weather is outstanding. I have my vaccine and getting ready to start travelling again. Next, I’d like you to meet Walter, our 25-pound ten weeks old German Shepherd. I am madly and deeply in love with him; if the little bugger lets me get a night’s sleep, I’d be even happier to see his fur face in the morning.

Over the years, dog owners I know have always compared owning a dog to having a baby; I get it, but you can’t lock a baby in a crate, or can you? I think we call it a playpen? All this to say, I can no longer look at my friends with the ya right expression on my face. As one puppy trainer compared a year with a puppy is like raising a ten-year-old in one year. You speed through the phases. My apologies to all the people I offended when I gave the ya right look on my face when they compared their puppy to a human baby; I now get it. Here’s hoping the getting up three times a night to pee ends soon; I need to sleep. But he is so adorable and so intelligent!!!

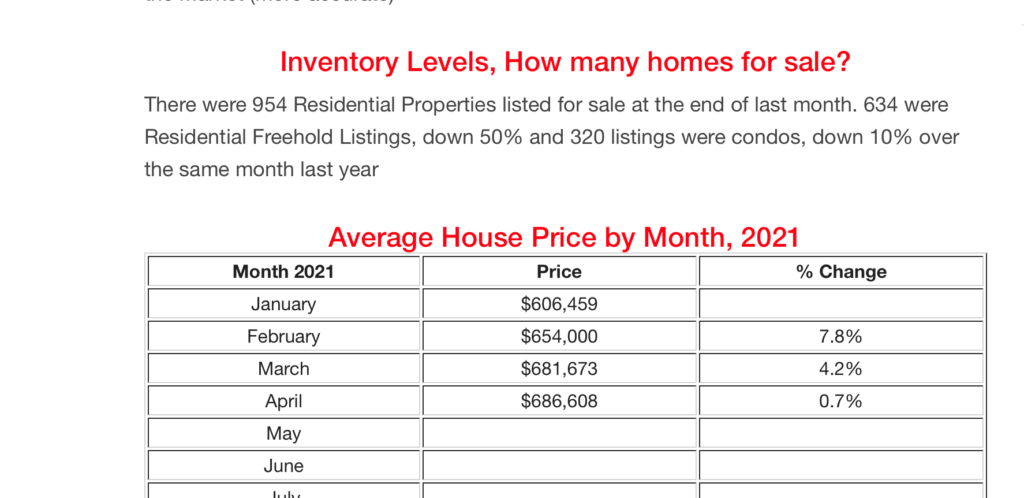

What’s going with the market. Well, pre-pandemic Ottawa, well, Canada had an inventory problem that really revealed itself as so many people tried to buy homes and ended up frustrated with the process, with some winning and others giving up. Whether it’s the roll-out of the vaccine and the world starting to open up, the gorgeous weather, the pricing of homes, the stress-test increase, or buyer fatigue, the market is showing signs of slowing. Thank Goodness!

What does this mean? Who knows, this is uncharted territory. My best guess is that we still have an inventory problem, so prices will not fall anytime soon, but you may have a better chance at getting a home? I’m starting to see contracts that show the scratches of negotiations and the return of conditions, I never thought I’d be so happy to see scratched-out numbers on an offer, but they are back. Maybe life buffers are helping out?

If you are thinking of reentering the market and needing to revisit your financing, call; let’s discuss the options available.

Fixed Vs Variable

What’s better, a fixed rate or a variable/adjustable rate?

Before I answer this question, you must understand the difference between a fixed-rate mortgage, adjustable-rate, and a variable rate mortgage.

An educational moment is coming up.

Fixed-rate mortgage: – A fixed-rate mortgage offers a specific interest rate that is fixed or “locked-in” for the term of the mortgage. The amount of your regular mortgage payments is consistent, as is the portion of your payment that goes toward principal and interest. The majority of Canadians typically use a five year fixed term.

Pro: you have the comfort of knowing that the payment never changes.

Con – depending on your goals, you may be paying too much in interest? Especially in the first two years.

Adjustable-rate mortgage: An “Adjustable Rate Mortgage” or ARM refers to the type of mortgage where the interest rate and mortgage payments will rise and fall with the prime lending rate. The lender’s prime rate typically follows the Bank of Canada. I say, typically because when the Bank of Canada rate is reduced by the Governor of the Bank of Canada, lenders do not always follow suit.

Variable-rate Mortgage: A variable rate mortgage will fluctuate with the Prime rate throughout the mortgage term. While your regular payment will remain constant, your interest rate may change based on market conditions. And the fluctuation will impact the amount of principal reduction you receive each month. When rates are low, more of your payment will be directed towards the principal, and when the interest rates are higher, a larger percentage of your monthly mortgage payment will go towards the interest portion of your loan.

As long as the interest portion stays below your required payment, your payment will not vary. If rates rise and the interest portion increases above your natural payment, your mortgage payment will increase.

Which one is better for you?

I’m shrugging my shoulders. Only you can make this decision.

Here’s a quick test:

Do you lose sleep when it comes to money?

If your payment was to change, would it cause anxiety?

Are your overall finances a source of stress or concern?

Then an adjustable rate or a variable rate mortgage might now be right for you?

We can discuss options; there’s no one size fits all.

Oh, did you know that an increase/decrease of 0.25% is equal to $12.10 on $100,000.00? Yep, that means if you have a $300,000.00 mortgage and Prime went up by 0.25%, your monthly mortgage payment will increase by $36.00. My job is to take the fear away and bring understanding. When we have a better understanding, we make informed decisions.

Would you like to go deeper?

A study by Moshe Arye Milevsky tracking interest rates from 1950 – 2000 revealed that consumers were better off, on average, financing a mortgage with a variable rate compared to a long term fixed-rate mortgage. A consumer with a $100,000 mortgage and an average amortization period of 15 years would pay $22,000 more in interest renewing with a five-year rate instead of using an adjustable-rate mortgage.

Thoughts:

You cannot lock into the adjustable rate. That’s the difference between a fixed-rate and an adjustable-rate. The rate stays the same – for better or for worse. And adjustable-rates changes – for better or for worse. You can rollover to a fixed rate and lock-in to whatever the fixed rate is at the time.

Having an adjustable-rate means, you receive the good times AND the not so good times. When Prime or the Bank of Canada rate goes up, so will your mortgage rate and payment. When the Prime or the Bank of Canada rate decreases, you *MAY* see your rate and mortgage payment go down the month following the decrease, provided the lender that your mortgage is placed with also lowers their Prime lending rate.

You’ll notice that there’s an *asterisk* there. Just because the Bank of Canada lowers, the rate does not mean the lender will follow. For example, The Bank of Canada Rate is currently .25%, and yet the bank Prime rate is 2.45%; what’s up with that?

The math 0.25% BoC rate + 2% Lender increase = 2.25% Which means that Prime should be 2.25% logically, right? WRONG. The lenders did not trickle down those deceases to the consumer.

The Bank of Canada lends the money out to the banks. It is called the overnight lending rate. Then the lender (one of the Big six banks) adds 2% to the Bank of Canada rate, which becomes the Prime lending rate. The Prime Rate is the rate that the banks use to lend to consumers. Be mindful; two of the green colour lenders have their Prime rate higher than the other lenders.

The Bank of Canada announces changes to the Overnight lending rate eight predetermined and fixed dates a year.

Yes, the BoC could increase or decrease the rates as they see practical and helpful to the economy. I do not see the Finance Minister or the Governor of Bank of Canada increase rates with the same vigour as they did in the 1980s. It would be political and economic suicide.

Because nothing is straightforward, of course, all rates will depend on the mortgage you are considering. Are you buying, refinancing, or transferring a mortgage? The rates for a CMHC insured mortgage are not the same for some refinancing their home to release equity for a renovation. Having an experienced broker on your side is essential to getting you to your goals.

If you would like to discuss what type of mortgage will help you with your financial, budgetary, and housing goals, call me. I am here to help.

Residential Market Commentary – Inflated inflation forecast – First National Financial LP

Much of the economic talk so far this year has centered on interest rates. The main questions have been when will they start to rise and by how much. In an attempt to provide answers economists and analysts monitor a key factor that guides interest rate policy: inflation.

Inflation has been a non-issue in North America for the better part of 40 years. That’s largely because after the last significant bout of inflation, in the late ‘70s through the mid ‘80s, central banks in Canada and the U.S. were given the job of keeping it under control. At that time the Bank of Canada rate topped 21%, and mortgage rates looked more like credit card interest.

Interest rates are the traditional tool used to control inflation. When it is deemed to be too low, and the economy stops growing, rates get trimmed to stimulate demand and spending. When inflation is too high, rates are raised in an effort to cool off the economy.

Over the past month or so inflation has jumped up in both Canada and the U.S. In March, Canada’s Consumer Price Index hit 2.2% on an annualized basis. Up from 1.1% in February. In the U.S., April’s CPI came in at 4.2%. It was enough to rattle American stock markets, which experienced significant drops, at least for a day or two.

But one month does not make a trend and there are mitigating factors. The increases in both countries are compared to the pandemic slump of a year ago. The corresponding employment reports on both sides of the border were weak. (Strong employment tends to drive inflation because more people have more money to spend.) And, both the Bank of Canada and the U.S. Federal Reserve have been expecting inflation spikes as COVID restrictions are loosened. Both have said they will not be responding to these temporary increases.

The central banks are watching for sustained, core inflation in the 2.0% range. The Consumer Price Index covers a broader range of products, including volatile items like food and fuel, that are factored out of central bank calculations. Home prices are not part of the calculation either. Houses are considered assets, not consumer goods.